Weekly Steel Market Pulse: Momentum Rebounds Across Flat and Long Products

Weekly Steel Market momentum returned to the metals complex this week, with almost every flat- and long-product benchmark posting healthy gains. Iron-ore’s futures-driven rally, coupled with renewed mill restocking in China, set a bullish tone that filtered through billets, wire rod and rebar.

Hot- and cold-rolled coils tracked firmer Asian import appetite, while stainless 304 coils outshone the pack on nickel’s ongoing surge.

Aluminium joined the advance, buoyed by fund inflows and shrinking LME warehouse inventories. Scrap HMS 2 into Turkey was the lone hold-out, as softening bids neutralised an early uptick. The snapshot below distils the week-on-week shifts and the intelligence behind them, giving you a concise pulse on this Weekly Steel Market.

Week-on-week price movement

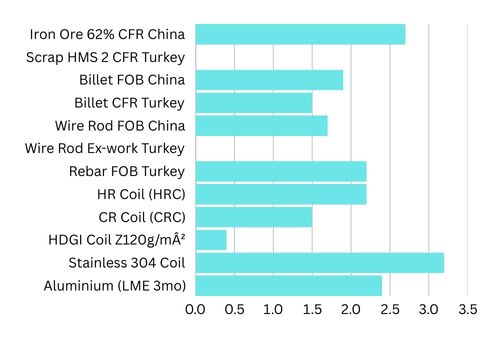

(Cumulative change from Mon 12 May → Fri 16 May 2025, derived from daily Mysteel, SteelOrbis, Platts, Fastmarkets & LME snapshots)

| Product | Direction | W/W Change % | Market Insight |

| Iron Ore 62 % CFR China | ▲ | +2.70 % | Futures-led rally and active mill restocking outweighed mid-week inventory pressure. |

| Scrap HMS 2 CFR Turkey | → | 0.00 % | Early-week uptick was neutralised by softer offers as Turkish buyers cooled. |

| Billet FOB China | ▲ | +1.90 % | Rising input costs and steady SE-Asian demand kept export offers firm. |

| Billet CFR Turkey | ▲ | +1.50 % | Middle-East and North-African buying interest lifted prices through the week. |

| Wire Rod FOB China | ▲ | +1.70 % | Tight supply and gradual SEA enquiries pushed offers higher. |

| Wire Rod Ex-work Turkey | → | 0.00 % | Domestic market remained lethargic; prices held flat all week. |

| Rebar FOB Turkey | ▲ | +2.20 % | Export rebound driven by North-African procurement and firmer billet costs. |

| HR Coil (HRC) | ▲ | +2.20 % | Improved Asian import appetite and futures strength underpinned gains. |

| CR Coil (CRC) | ▲ | +1.50 % | Followed HRC higher, though trading volumes stayed modest. |

| HDGI Coil Z 120 g/m² | ▲ | +0.40 % | Mills held minimum offers; small uptick on selective bookings. |

| Stainless 304 Coil | ▲ | +3.20 % | Nickel’s sustained rally translated into the strongest weekly rise in stainless. |

| Aluminium (LME 3-mo) | ▲ | +2.40 % | Fund inflows and falling warehouse stocks buoyed LME prices. |

Weekly Steel Market Highlights

Weekly Steel Market Sentiment

- US-China tariff pause energizes investors, sparking broad steel price rallies across exchanges.

- Indian metal stocks jump over eight percent, reflecting improved confidence. ( Economic Times )

- Market mood stays optimistic, yet analysts warn gains may fade when tariff grace ends.

- Moody’s still predicts soft iron ore prices because supply remains abundant.

Commodity Price Snapshot

- Iron ore September contract climbed seven percent to around ninety-nine dollars per ton.

- Shanghai rebar and hot-rolled coil futures advanced about one-and-a-half percent.

- Stainless steel futures gained slightly, but falling nickel prices capped broader upside.

- North American Stainless added a tariff surcharge, cushioning its 304 alloy price drop.

Regional Weekly Steel Market Highlights

- China’s steel demand shifts toward manufacturing and infrastructure, offsetting property slowdown. ( Metal Miner )

- Jiangsu province targets six-million-ton output cut, though compliance appears uncertain.

- Taiwan’s stainless market stays flat despite rising Chinese prices. ( Yieh Corp )

- Turkey’s coated steel prices fall amid weak domestic sales and export orders. ( Steel Orbis )

- ASEAN faces surging Chinese imports, prompting talks on protective measures.

Weekly Steel Market Opportunities and Risks

- Global rebar market projected to reach three-hundred-thirty billion dollars by 2034, growing 4.5 percent annually.(Market.Us)

- Asia Pacific dominates rebar demand, with Vietnam expanding fastest at eighteen-percent CAGR.

- Infrastructure spending, especially India’s multi-trillion-rupee program, sustains steel consumption momentum.( Economictimes)

- Persistent iron ore oversupply and uncertain Chinese output cuts could pressure prices later.

- Watch policy shifts after ninety-day tariff truce; extension or rollback will steer Weekly Steel Market dynamics.

MCB – Summary Of Treasury Market Report – 16-05-2025

FX and Rates Snapshot

- FX option volatility climbed, signalling trader caution as markets watch President Trump’s Middle East visit.

- Dollar Index held near 100.65, while EUR-USD and GBP-USD stayed stuck in tight, range-bound trading zones.

- Two-year US Treasury yield slid sharply, deepening curve steepening and boosting expectations for September Fed rate cuts.

US Economic Outlook

- April data showed weaker producer prices, manufacturing output and core retail sales, confirming a broader economic slowdown.

- Traders now price at least two Fed cuts for 2025, assigning 75 percent odds to a September start.

- University of Michigan consumer sentiment ticked up slightly, but remains historically low because of policy and inflation worries.

Emerging-Market Highlights

- Bank of Uganda bought dollars and used swaps to rebuild reserves, aiming for four billion dollars by December.

- Malawi’s IMF credit-facility collapsed after fiscal slippage, clouding debt restructuring plans and future external funding.

- Rwanda kept its policy rate at 6.5 percent and will begin gold purchases in July to diversify reserves.

Commodity Trends

- IEA lifted 2025-26 oil demand growth forecasts on stronger GDP assumptions and cheaper crude.

- Copper prices edged higher, supported by a temporary US-China tariff truce, though long-term demand doubts persist.

- EU wheat and barley crop outlook improved overall, but northern Europe drought still threatens yields.

Key Levels to Watch

- USD-JPY found importer support below 145.00, yet overall momentum remains downward.

- Mauritius Treasury-bill auctions saw yields stable within a narrow corridor.

- Aluminium prices not covered today; focus stayed on copper and energy markets.

Weekly Steel Market Wrap-Up: Key Signals and Next Week’s Watchpoints

This week’s Weekly Steel Market shows broad strength across almost every product category, driven by iron-ore and restocking demand.

Flat products followed rising Asian imports, while long products gained on tight supply and recovering export orders.

Stainless outperformed as nickel rallied again; aluminium mirrored the bullish mood amid shrinking inventories.

Scrap prices stayed flat, reminding participants that demand signals remain mixed despite stronger futures sentiment.

Monitor Chinese restocking pace, regional billet flows, and nickel trajectory to gauge whether this momentum can extend next week.

Need a tailor-made procurement game-plan?

Our team at Star Trading Global tracks every cargo, policy shift and futures print in real time.

Message us or hit “Contact” below for:

• Person-specific market briefings

• Benchmark comparisons without disclosing your price

• Forward-coverage strategies that protect margins