Weekly Steel Market Overview: Key Trends & Price Movements

Weekly Steel Market trends dominate the spotlight this week, revealing how shifting trade policies and strong demand shape global price movements.

China’s booming metals market contrasts weaker global prices, while US tariffs stir uncertainty across the Weekly Steel Market, influencing trade flows worldwide.

To help you quickly grasp trends in the Weekly Steel Market, we’ve prepared a table and bar chart showing recent price movements.

The data below highlights week-on-week changes from July 7 to 11, helping you spot which metals led gains or stayed flat.

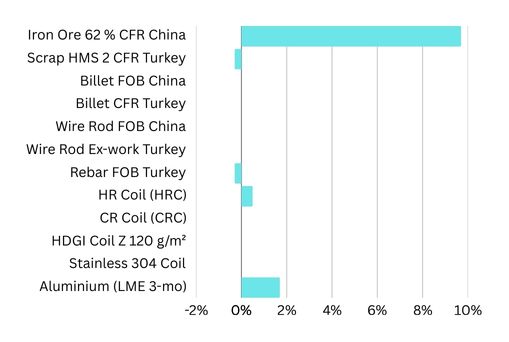

Week-on-week price movement

(Mon 7 → Fri 11 July 2025 – cumulative change)

| Product | Direction | W/W Change % | Market Insight |

|---|---|---|---|

| Iron Ore 62 % CFR China | ▲ | +9.7 % | Monday’s policy-driven spike (+11 %) was only partly unwound by two mild pull-backs mid-week. |

| Scrap HMS 2 CFR Turkey | ▼ | -0.3 % | Turkish mills paused fresh bookings after a brief early-week uptick. |

| Billet FOB China | → | 0.0 % | Chinese exporters kept offers flat on balanced domestic/export demand. |

| Billet CFR Turkey | → | 0.0 % | MENA buyers stayed on the sidelines, leaving import prices unchanged. |

| Wire Rod FOB China | → | 0.0 % | Tight billet supply kept export rod offers locked in all week. |

| Wire Rod Ex-work Turkey | → | 0.0 % | Local demand remained muted, resulting in no net price move. |

| Rebar FOB Turkey | ▼ | -0.3 % | A small mid-week dip (-0.28 %) on softer July enquiries set the tone. |

| HR Coil (HRC) | ▲ | +0.5 % | U.S. futures rebound (+1.1 % Wed) outweighed Thursday’s slip. |

| CR Coil (CRC) | → | 0.0 % | Tracked HRC but closed the week flat. |

| HDGI Coil Z 120 g/m² | → | 0.0 % | Coated-coil exporters reported minimal inquiry, keeping offers steady. |

| Stainless 304 Coil | → | 0.0 % | Nickel’s calm tone translated into unchanged stainless prices. |

| Aluminium (LME 3-mo) | ▲ | +1.7 % | Three modest daily gains (+0.82 %, +0.54 %, +0.30 %) stacked up as inventories kept shrinking. |

Global Steel and Weekly Steel Market Highlights – July 2025

Weak Dollar Lifts Metal Prices

- A weaker US dollar at 97.38 helped push global metal prices higher, boosting demand from buyers in other currencies.

- Zinc, nickel, and tin prices climbed on both SHFE and LME, though SHFE copper dropped slightly due to property concerns.

- Precious metals like gold and silver rose modestly as safe havens during times of currency volatility.

China’s Steel Market Momentum

- Baosteel raised carbon steel flat product prices by RMB 100/mt for August deliveries, showing rising confidence in demand.

- Chinese HRC prices rose $3-6/mt on July 11, driven by expected capacity cuts and strong industrial activity.

- Steel futures in China climbed to CNY 3,090 per tonne, while production cuts in Shanxi may remove 6 million tonnes.

- Coking coal and coke prices jumped over 3%, with some plants planning more hikes to support higher steel costs.

- Finished steel inventories fell, and China’s construction PMI hit a three-month high, signaling steady end-user demand.

Turkish Steel Market Faces Weak Demand

- Turkish flat steel prices stabilized after sharp declines, but demand remained weak, forcing sellers to offer discounts.

Nippon Steel’s Global Expansion

- Nippon Steel plans to double US crude steel production, modernizing US Steel’s plants with an $11 billion investment by 2028.

- Its global target is 100 million mt annually, aiming to avoid reliance on China and expand in India, Thailand, and Slovakia.

China’s Automotive and Resource Push

- China’s new energy vehicle sales exceeded 6.9 million units in H1 2025, accounting for over 44% of total vehicle sales.

- China discovered 38 new mineral sites, boosting domestic resource security and reducing reliance on imported critical minerals.

Global Trade and Shipping Resilience

- European container shipping rates rose 1.62%, signaling strong global trade despite geopolitical tensions and Red Sea route diversions.

- China’s auto exports grew 10.4% YoY, with NEV exports surging 75.2%, keeping trade flows robust despite tariff concerns.

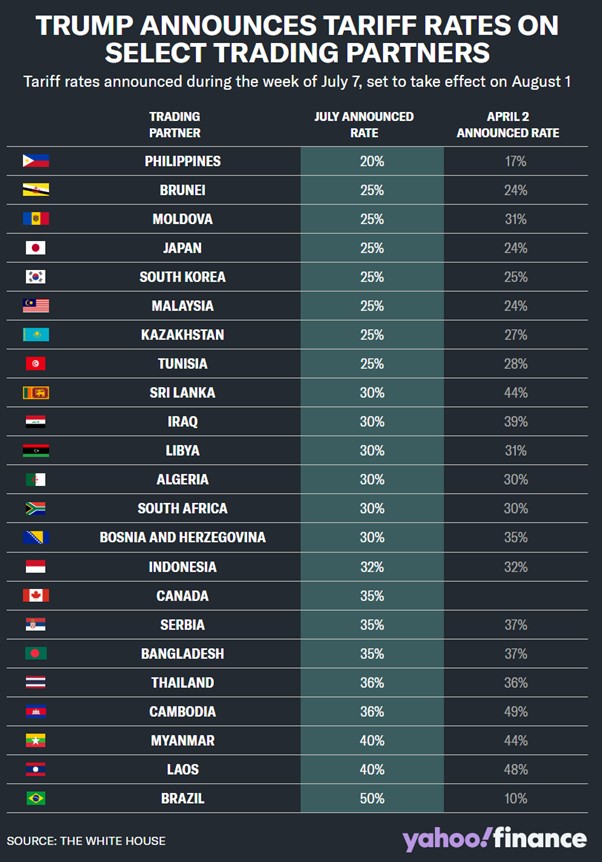

US / Trump Tariff Update – Steel Market Impact

New Copper Tariffs Announced

- The US will impose a 50% tariff on imported copper from August 1, matching existing tariffs on steel and aluminium.

- COMEX copper prices jumped 2.4% after the announcement, showing market concern over supply chain disruptions and cost increases

Wider Tariff Scope and Trade Shifts

- The US is applying tariffs of 20-50% on goods from many countries, including Canada (35%) and Brazil (50%).

- Vietnam secured a 20% tariff, with 40% for transshipped goods, while the EU seeks exemptions for key industries.

- India is negotiating lower tariffs under a new framework deal to maintain access to the US market.

Economic and Policy Implications

- Trump’s tariffs could delay expected US interest rate cuts to September, adding uncertainty to financial and commodity markets.

- Higher tariffs may raise prices for US consumers and prompt shifts in global steel trade flows, impacting the Weekly Steel Market.

Outlook and Takeaways: Navigating Weekly Steel Market Shifts

In conclusion, this Weekly Steel Market update shows how China’s gains, shifting trade policies, and steady demand shape global price trends.

Iron ore surged on policy support, aluminium rose on low stocks, while other products held steady, reflecting cautious buyer sentiment.

Trump’s new tariffs and ongoing negotiations could still reshape trade flows and price dynamics in the Weekly Steel Market ahead.

Staying informed about production shifts, global policies, and market signals remains essential for navigating the steel industry confidently in coming weeks.

Need a tailor-made procurement game-plan?

Our team at Star Trading Global tracks every cargo, policy shift and futures print in real time.

Message us or hit “Contact” below for:

• Person-specific market briefings

• Benchmark comparisons without disclosing your price

• Forward-coverage strategies that protect margins