Weekly Steel Market Trends: Output Declines & Trade Shifts

Weekly Steel Market dynamics shifted again as falling April output met volatile trade flows and fresh tariff threats.

Global crude steel production slid in April, India turned net importer, and stainless inventories stayed stubbornly high.

Raw-material prices held steady, yet demand signals stayed weak, keeping most benchmarks rangebound despite minor rallies.

Across the Weekly Steel Market, attention now pivots to China’s restocking pace and the potential shock from proposed Trump tariffs.

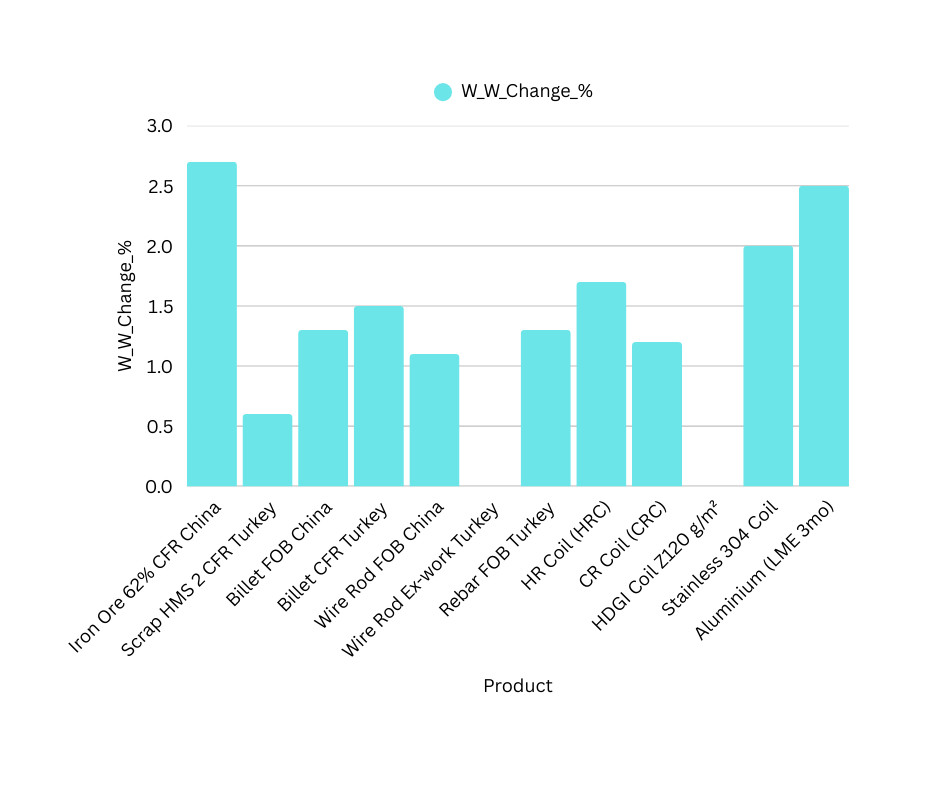

To provide a clearer view of short-term pricing momentum, we’ve compiled a week-on-week summary of key steel and metal product movements from May 19 to May 23, 2025.

The table below highlights directional trends, percentage changes, and brief market insights based on data from Mysteel, SteelOrbis, Platts, Fastmarkets, and the LME. A corresponding bar chart follows to help you visualise which segments led the gains in this week’s Weekly Steel Market.

Product | Direction | W/W Change % | Market Insight |

| Iron Ore 62 % CFR China | ▲ | +2.7 % | Ongoing mill restocking and firm futures kept iron-ore prices on an upward trajectory all week. |

| Scrap HMS 2 CFR Turkey | ▲ | +0.6 % | Mid-week Turkish buying revived scrap values after a flat start. |

| Billet FOB China | ▲ | +1.3 % | Export offers held firm on elevated input costs and consistent SE-Asian demand. |

| Billet CFR Turkey | ▲ | +1.5 % | Steady MENA procurement supported billet import prices through the week. |

| Wire Rod FOB China | ▲ | +1.1 % | Tight billet supply and cost push lifted wire-rod quotes. |

| Wire Rod Ex-work Turkey | → | 0.0 % | Domestic Turkish market remained lethargic, leaving prices unchanged. |

| Rebar FOB Turkey | ▲ | +1.3 % | North-African buying interest and firmer billet costs kept rebar exports trending higher. |

| HR Coil (HRC) | ▲ | +1.7 % | Restocking in South & SE Asia sustained HRC’s week-long climb. |

| CR Coil (CRC) | ▲ | +1.2 % | CRC followed HRC higher, though gains were more muted amid thin trading. |

| HDGI Coil Z 120 g/m² | → | 0.0 % | Export offers stayed flat as international demand remained subdued. |

| Stainless 304 Coil | ▲ | +2.0 % | Robust nickel prices continued to fuel stainless steel’s outperformance. |

| Aluminium (LME 3-mo) | ▲ | +2.5 % | LME contract strengthened on falling inventories and renewed fund inflows. |

Weekly Global News & Highlights

Global Production Trends

- Global crude steel output fell 6.3 % month-on-month to 155.7 Mt in April, down 0.3 % year-on-year. ( GMK Centre)

- Year-to-date production slipped 0.4 % versus 2024, signalling a cautious supply environment.

- China stayed flat, India grew 5.6 %, while Japan, Russia, Germany and Brazil each contracted.

India’s Shifting Trade Flows

- Finished steel imports declined 11.3 % after a 12 % safeguard duty curbed cheap inflows.(Reuters)

- Imports from China and Japan dropped sharply; France and Germany surged on plate cargoes.

- Steel exports fell 25.7 %, leaving India a net importer during April.

Stainless and Construction Steel Snapshot

- Stainless transactions remained sluggish; inventories stayed high despite a minor weekly drawdown.

- Wuxi destocked slightly, while Foshan built stock, keeping overall pressure intact.

- Construction steel prices fluctuated in a narrow band amid weak demand and steady supply. (SMM)

Raw-Material Signals

- Ferrochrome tenders held flat; rising output hints at future surplus despite firm ore support.

- Domestic iron-ore concentrate prices inched higher; futures still muted though sentiment brightened post-policy briefing.

- Turkish flat-steel prices held steady, yet market mood remains gloomy on limited orders. ( Steel Orbis )

Trump Tariff Watch

- Trump threatened 25 % tariffs on non-US-made iPhones and similar levies on other smartphone brands by June 2025. ( Yahoo Finance)

- He proposed a “straight 50 %” tariff on all EU imports from 1 June 2025, rejecting further negotiation.

- EU prepares $108 billion in retaliatory duties; escalation could disrupt trans-Atlantic steel trade flows.

Weekly Steel Market Outlook

- High inventories and guarded demand suggest prices remain rangebound, with rallies capped by cautious buying.

- Monitor Chinese restocking, raw-material moves and Trump tariff developments to gauge next-week direction.

Weekly Steel Market Wrap-Up

In conclusion, this Weekly Steel Market update reflects a cautious global environment shaped by weaker output, shifting trade flows, and policy risks.

While some raw materials remain stable, high inventories and soft demand continue to limit upside in both flat and long steel products.

Trump’s tariff threats against the EU and tech giants may add further volatility, especially if retaliatory measures disrupt trade routes.

Market participants should closely monitor Chinese restocking, raw material pricing, and tariff developments to navigate the weeks ahead with clarity and confidence.

Our team at Star Trading Global tracks every cargo, policy shift and futures print in real time.

Message us or hit “Contact” below for:

• Person-specific market briefings

• Benchmark comparisons without disclosing your price

• Forward-coverage strategies that protect marginsStay ahead of the curve—Sourcing Strength , Delivering Trust